Tips On Obtaining One Of The Most Out Of Your Home Mortgage

Content by-Mercado CrossIf you're looking into home mortgages, then you surely are excited. It's time to buy a home! However, what you might realize is there is quite a lot of information to take in, and how do you sort all of this out to get to the mortgage company and product that you need? Keep reading to find out how to do this.

Consider unexpected expenses when you decide on the monthly mortgage payment that you can afford. It is not always a good idea to borrow the maximum that the lender will allow if your payment will stretch your budget to the limit and unexpected bills would leave you unable to make your payment.

There are additional resources for first time home buyers. These loans usually do not require a lot of money down and often have lower interest rates than standard mortgages. Most first time home buyer loans are guaranteed by the government; thus, there is more paperwork needed than standard mortgage applications.

Get mortgage loan estimates from at least three different mortgage lenders and three different banks. By shopping around, you may get a lower interest rate, pay fewer points and save money on closing costs. It's almost always preferable to get a fixed interest rate. With what is it worth , you may not know from month to month what your mortgage payment will be.

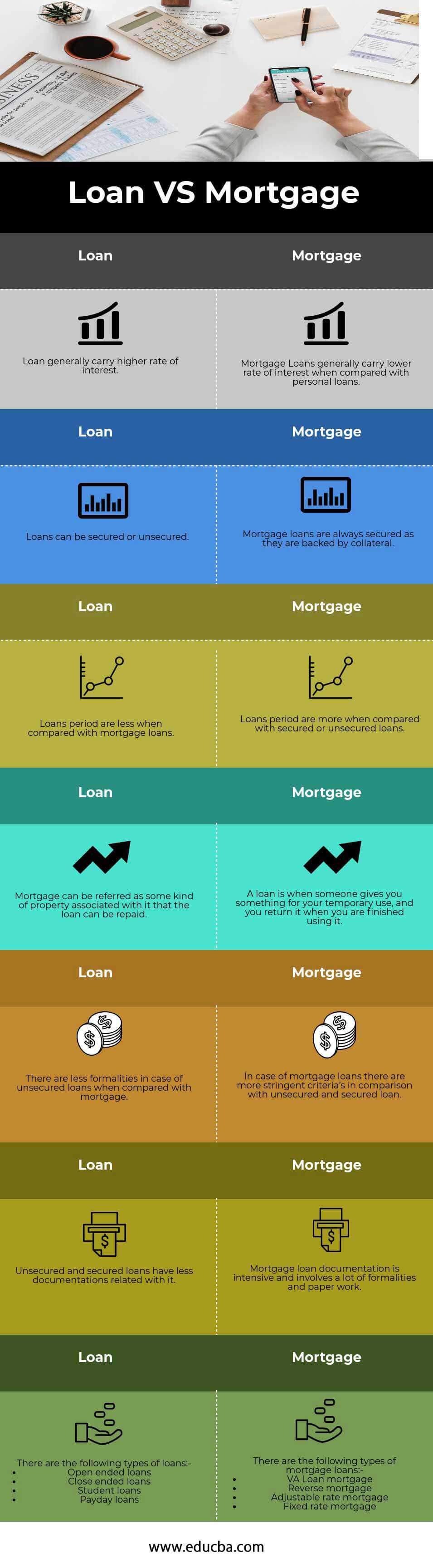

Know your credit score and verify its accuracy. Identity theft is a common occurrence so go over your credit report carefully. Notify the agency of any inaccuracies immediately. Be particularly careful to verify the information regarding your credit limits. Make all your payments in a timely manner to improve your score.

If you are a veteran of the U.S. Armed Forces, you may qualify for a VA morgtage loan. These loans are available to qualified veterens. The advantage of these loans is an easier approval process and a lower than average interest rate. The application process for these loans is not often complicated.

One type of loan that is not normally talked about is an interest only loan. This type of loan allows you to make low monthly payments for a certain period, then the payment amount increases. These loans are generally used to help you get into a home at a low monthly payment.

Save your money. When you are going to finance a home mortgage, you will need to have some cash for a down payment. The more money you pay down, the lower your payments and interest rates. The down payment goes directly to the principal of the mortgage and is a sum you will not owe yearly interest on.

Think about your job security before you think about buying a home. If you sign a mortgage contract you are held to those terms, regardless of the changes that may occur when it comes to your job. For example, if you are laid off, you mortgage will not decrease accordingly, so be sure that you are secure where you are first.

Be sure to have all your paperwork in order before applying to a lender. You will need to have good documentation of your income, your tax status and your financial obligations. Ask each lender you intend to apply with exactly what is needed for a successful application. Gather your documentation accordingly so that your home mortgage application process will be smooth, simple and successful.

Keep your credit score in good shape by always paying your bills on time. Avoid negative reporting on your score by staying current on all your obligations, even your utility bills. Do take out credit cards at department stores even though you get a discount. You can build a good credit rating by using cards and paying them off every month.

You may be so excited about getting a new home that you go out and start buying all types of furniture. Unless you are paying for the furniture in cash, you need to hold off on this. You don't want to open any lines of credit or make any large purchases until after your loan is closed.

If you are a retired person in the process of getting a mortgage, get a 30 year fixed loan if possible. Even though your home may never be paid off in your lifetime, your payments will be lower. Since you will be living on a fixed income, it is important that your payments stay as low as possible and do not change.

Having a strong employment history will make it easier to qualify for a home mortgage. Lenders like to see that you have been at the same job for a good length of time. Barring that, they like to see continuous employment for at leas the past five or more years.

You should work to find a cosigner for your loan before applying. If you have anyone in your family with great credit, a business, history with the lender, etc, then having their signature alongside yours will put your application in a much better light. So seek out family, friends, business partners, and others who could cosign for you.

Know the real estate agency or home builder you are dealing with. It is common for builders and agencies to have their own in-house financiers. Ask the about their lenders. Find out their available loan terms. This could open a new avenue of financing up for your new home mortgage.

Ask around about mortgage financing. You may be surprised at the leads you can generate by simply talking to people. Ask your co-workers, friends, and family about their mortgage companies and experiences. They will often lead you to resources that you would not have been able to find on your own.

Look into credit unions. There are many options for obtaining financing and credit unions have their strengths. Often credit unions will hold mortgages in their private portfolio. Banks and other financial institutions routinely sell mortgages to other holding companies. This could result in your loan changing hands multiple times over its lifetime.

Now that you've made it to the bottom, there is only one thing left to do. Make use of this learning you have done today by seeking out an exceptional mortgage. It will be an easy process, now that you know so much, so get started as soon as possible.